Deficit reduction and growth are not alternatives. Delivering the first is vital in securing the second. If markets don’t believe you are serious about dealing with your debts, your interest rates rocket and your economy shrinks. … Those who argue we should spend more want us to borrow more, driving up our deficit and our debt and putting our hard-won credibility and low interest rates at risk.There’s a logic to it: if government borrowing goes up, then the markets will get worried about lending to it and charge a higher interest rate. That may not become a Greek-style debt spiral, but even so, more expensive borrowing costs the taxpayer more and makes cuts to public services more likely.

But are things working the way Cameron suggests?

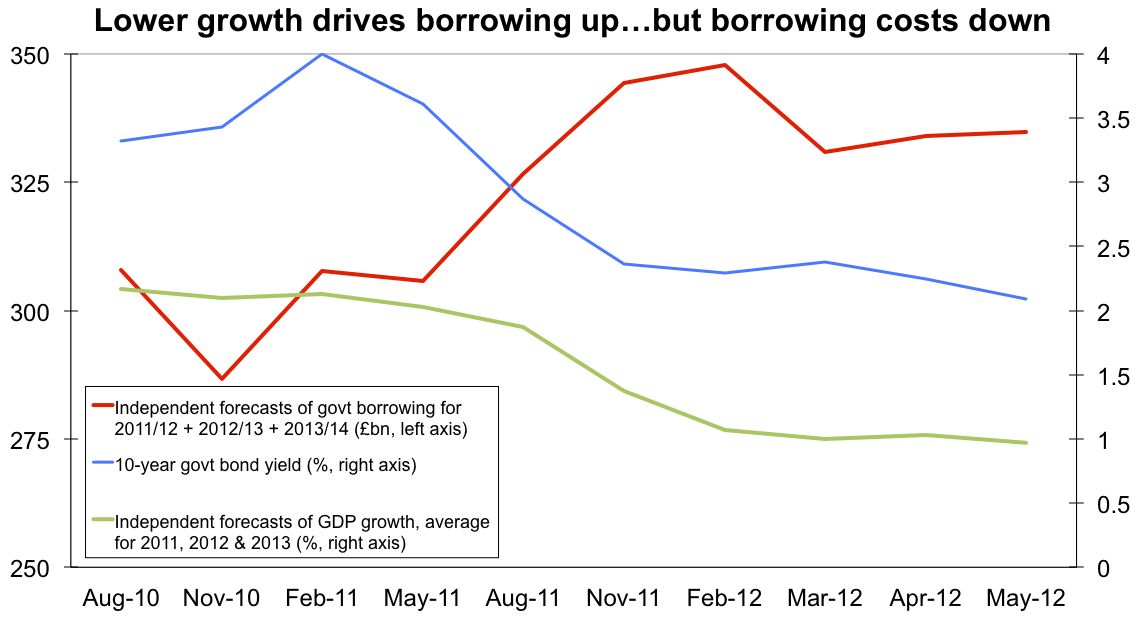

Not exactly. The amount of money that the government is expected to borrow over the next few years has gone up, not down. This rise in expected borrowing undermines Cameron’s claim that he is sticking fast to a plan that is working out well. The one thing he’s right about is that government borrowing costs have been falling. Oddly, these two changes have gone hand in hand.

This chart shows the yield on ten-year government bonds – a standard benchmark for the cost of borrowing – along with the changing independent economic forecasts of government borrowing over 2011/12 to 2013/14:

If the intuitive logic were right, you’d expect the two lines to rise and fall in tandem. But exactly the opposite happens (a strong negative correlation of –0.85). As the government’s plans for reducing borrowing get knocked farther off track, the markets become happier to lend to it more and more cheaply.

Why?

The answer is that the prospects for the economy have been getting worse. Here’s the same graph with the independent forecasts of GDP growth for 2011 to 2013 added in:

As you’d expect, when growth prospects go down, predicted government borrowing goes up (a correlation of –0.83).

But the worsening economy also means cheaper government borrowing (correlation +0.93). The reason for that is that as the private sector struggles to generate growth, investors become reluctant to buy corporate bonds. So they turn to government bonds, and the increased demand for these means that the government can get away with offering a lower interest rate.

International factors such as Greece are also relevant: investors flee crisis-hit countries’ government bonds and go for the relative safety of UK, US, German and Japanese bonds. But this was happening even before the 2010 election: under Brown and Cameron alike, the markets haven’t thought there was any real risk of the UK losing control of its debts and defaulting. For more on that, see my post from last November.

Cheap government borrowing may be good for the Treasury, but in the current circumstances it’s not a sign of ever-increasing confidence in the government’s plans (which are really not working out as well as hoped). It’s a sign that the private sector is so weak that nobody wants to invest in it.

1 comment:

Amazingly enough, the Pound has become a "safe haven", as has the dollar. I am not an economist, but I believe this has something to do with the UK controlling its own currency. Investors become more worried about "return of capital" then return on capital.

Post a Comment